How much cash you need to replicate the state pension

🔸 Plus: Neil Woodford is back, like it or not 🔸 Buying a real Christmas tree instead of a fake one is better for your mental health 🔸 What you get paid at London’s top 20 hedge funds 🔸

Your 2-minute guide to demystifying money and making you richer

The markets, year-to-date

S&P 500: 5,930.85 ⬆️ 25.41%

FTSE 100: 8,084.61 ⬆️ 4.94%

Bitcoin: $93,384.99 ⬆️ 111.26%

GBP to USD: 1.2532 ⬇️ 1.53%

GBP to EUR: €1.2030 ⬆️ 4.33%

(As of Friday market close.)

How much you’d need to save to replace the state pension

Most if not all Britons expect the government to look after them when they retire, in the form of the state pension. That’s the guaranteed cash benefit every Brit becomes entitled to at age 66. The state pension is currently worth £221.20 per week.

That’s £11,502.40 a year. The pension goes up each year via the infamous “triple lock”: a percentage increase that is the equivalent of the rise in average wages, or the inflation rate, or 2.5% — whichever of the three is greatest.

So, the state pension will be nice to have — it’s free money! — but it won’t be enough to live on.

This is one of the reasons we created Moneyin2: You’re going to need a backup plan.

One way to look at this is to ask, how much would you need to create a retirement nest egg that pays you the equivalent of the state pension?

The question isn’t straightforward because you don’t know how many years you’ll live for after age 66. Life expectancy is so good that many of us will have to plan for 30 years’ worth of cash. AJ Bell, the investment platform, estimates that most would need to save £250,000 by the time they retire to obtain the equivalent of the state pension.

That’s a daunting figure, for sure

One plausible way to get there would be to save £500 per month for 20 years, and hope that your investment gains compounded at 6% annually. That would top out at £232,675. It’s a plausible, albeit conservative, estimate because the S&P 500 index of stocks generally rises by 6-10% per year.

If you stayed invested after the 20th year, and your investment continued to gain 6% annually, your savings would throw off another £15,000 a year. Of course, you might want to follow the 4% rule just to be safe, which would give you £10,000 in the first year but larger sums after that (assuming your investment continued to grow at a rate greater than 4%).

How doable is this?

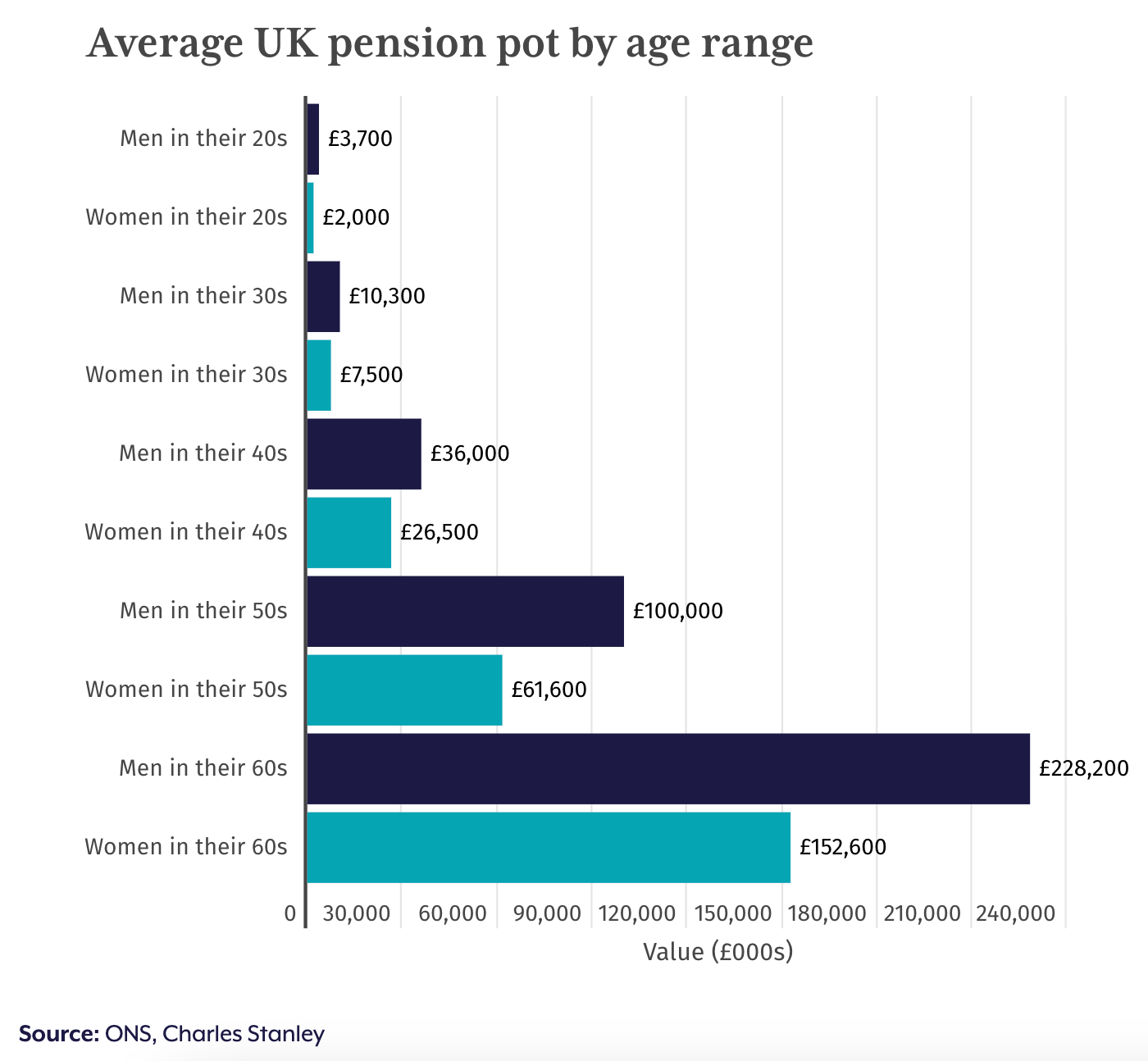

Charles Stanley, a financial advice firm, extracted the answer from the Office for National Statistics. By the time Brits hit their 60s, men have an average of £228,200 saved in their private pensions and women have £152,600. The difference is an effect of the gender pay gap — it has a severe effect on women’s savings.

Of course, that’s just pension savings. Those numbers don’t count non-pension savings like cash in the bank, ISAs, or money you could generate by selling your house.

Still, even if you socked away £250,000 you’re still looking at the equivalent of two state pensions — something like £22,000 a year. Again, that might not be enough. Adjust your personal target accordingly!

The key factor is time. These estimates use a short timeframe: Just 20 years. If you can plan around a longer horizon then getting there will be easier.

The Moneyin2 Guide to Wealth

The Moneyin2 Guide to Wealth will get you the biggest return on your savings by maximising cash matches from your employer, free cash from the government, and shielding your investment gains from tax. It takes you step-by-step through the world of pensions, SIPPs, ISAs and ETFs — all in plain English.

And for dessert …

Buying a real Christmas tree instead of a fake one is probably better for the environment and could (temporarily) improve your mental health, according to Joachim Klement.

Americans have bought more than 21 million “Elf on the Shelf” dolls but many parents are now lying to their kids because they want to end this “creepy” tradition.

What you get paid at London’s top 20 hedge funds. Average comp starts at $407.9K.

Neil Woodford, the investment manager whose £10 billion Woodford Equity Income fund collapsed to just £3.7 billion in June 2019, taking a lot of people’s retirement savings with it, has done another video trying to justify his actions.

More from Moneyin2:

Do you want Moneyin2 to recommend your Substack?

Get in touch at contact@moneyin2.com!

We want to hear from you!

What money issues do you want us to tackle in this newsletter? Let us know at contact@moneyin2.com.

Follow us on social media

Facebook, TikTok, Instagram, Twitter, and Threads.

Partner with us!

If you want to sponsor Moneyin2 get in contact here.

250k in today‘s money? That would be 450k in 20 years, assuming 3% inflation.