The 4% rule tells you how much you need to retire

🔸 Plus: Taylor Swift may have affected the UK inflation rate 🔸 What if AI doesn't make everything more productive? 🔸 Flipping a coin isn't a 50-50 bet 🔸

Your 2-minute guide to demystifying money and making you richer

The markets, year-to-date

S&P 500: 5,732.81 ⬆️ 20.87%

FTSE 100: 8,311.76 ⬆️ 7.64%

Bitcoin: $63,126.50 ⬆️ 42.81%

GBP to USD: $1.3078 ⬆️ 2.76%

GBP to EUR: €1.1911 ⬆️ 3.29%

As of Monday morning

The 4% rule

When people ask, “How much money do you need to retire?” The usual answer is, “it depends upon your individual circumstances”.

That, obviously, is incredibly unhelpful.

Luckily, there is a way to figure out exactly how much you, personally, will need using a simple formula that works for everyone:

Calculate your annual expenses.

Assume you’ll need 25 times that amount, for 25 years.

(This sounds like a lot — how the heck are you going to save 25 years of expenses?! But remember that you’re going to benefit from the gains on your investments along the way, tax breaks on your investments, and you’ll get help from the state pension.)

Assume you will draw down 4% of your savings every year. (Because 100% of your money divided by 4% each year equals 25 years to get to zero.)

Doing this should give you enough money for 30-plus years of retirement.

Why does 25 years’ worth of money last for 30 years or more?

Because your savings and investments will continue to earn returns during your retirement, stretching your savings further even while you are drawing them down.

If stocks give you a 6-10% annual return on average, then taking only 4% a year gives you a margin of safety. In theory, your underlying portfolio will continue to grow even though you are withdrawing from it.

This is called “the 4% rule” and it is based on decades of research on sustainable withdrawal rates from retirement portfolios.

The safety margin is important because in some years your portfolio is likely to decline. This is called the “sequence of returns risk”. It describes the danger that retirees can get into if their portfolios decline, especially in the early years of retirement. While it’s comforting to think your savings will always grow by 6-10% a year, the reality is that in some years they might decline by 20% or more.

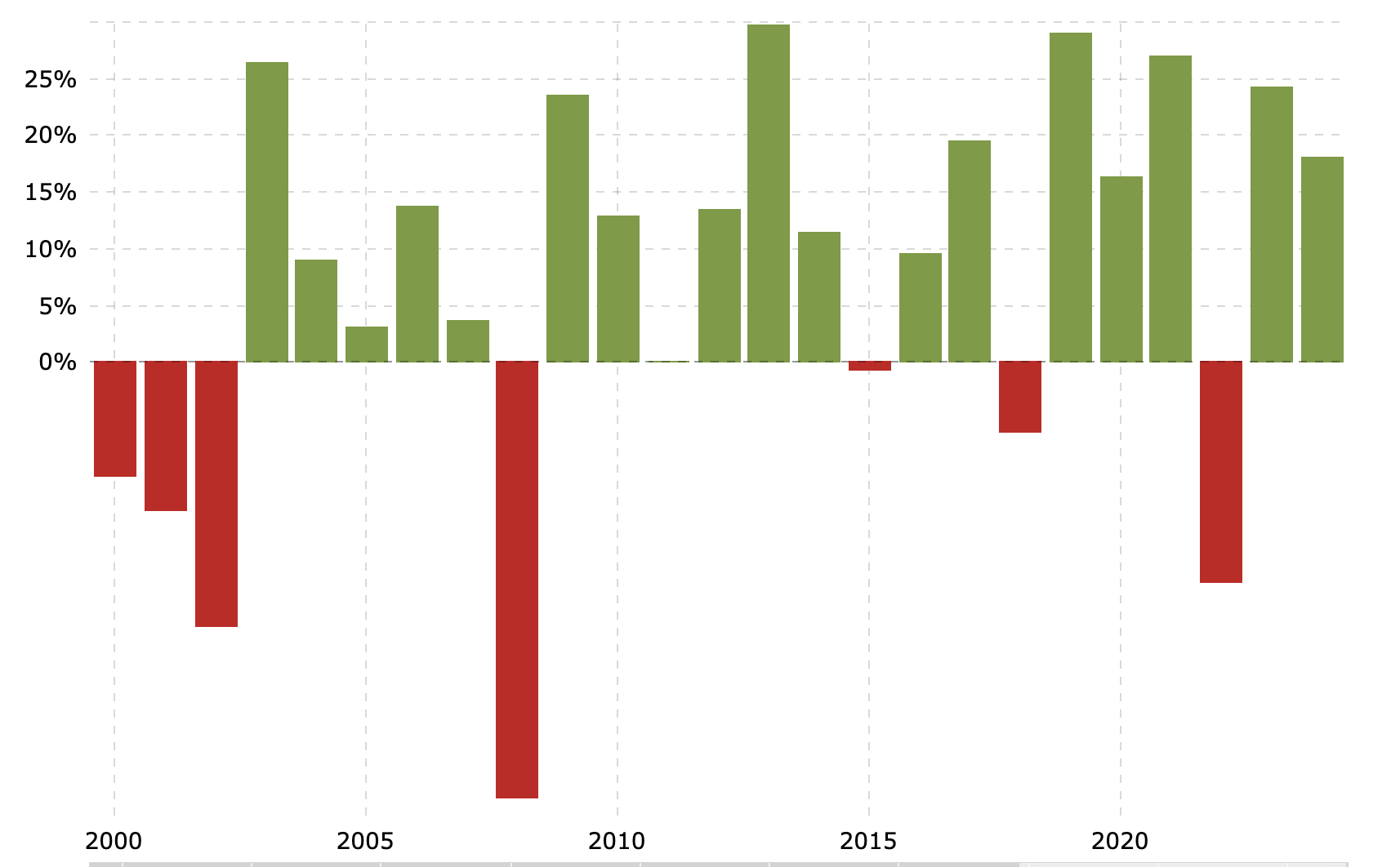

Here are the S&P 500’s annual returns since 2000:

Clearly, anyone who retired in 2008 took an immediate, massive hit. But the years that followed were robust, and the 4% rule would have let their savings grow and grow.

There’s a great article here explaining how sequencing risk can hurt you if you do not have that safety margin.

The other reason to follow the 4% rule is that it’s relatively conservative

A 4% drawdown rate will take you through a worst-case scenario in which you deplete your savings entirely. But in most cases, someone following the 4% rule would end up with more money than when they started, precisely because a standard mixture of stocks and bonds tends to return 6-10% per year on average.

If you want more detail on the 4% rule here are some helpful articles:

How Much Is Enough? - by Bill Bengen, the inventor of the 4% rule.

How Much Money You Need For Retirement - by Ben Carlson.

How To Understand Sequence of Returns Risk - by Rob Berger and Benjamin Curry.

The Extraordinary Upside Potential Of Sequence Of Return Risk In Retirement - by Michael Kitces.

What If The 4% Rule For Retirement Withdrawals is Now the 5% Rule? - by Ben Carlson

What Is the 4% Rule for Withdrawals in Retirement: How Much Can You Spend? - by Julia Kagan

And for dessert …

The high price of Taylor Swift tickets probably affected the UK’s rate of inflation, according to Deutsche Bank.

What if AI doesn’t change everything? An MIT economist’s claim that artificial intelligence won’t usher in a new era of productivity growth is getting attention.

Flipping a coin isn’t exactly a 50-50 bet. A study shows: “Coins are tossed in air, not in a vacuum and the physics of the air turbulence around a rotating coin are such that it becomes slightly more likely that it will land the same side up as it started. Second … because of a slight misalignment of the flipping finger, the tossers create a slight bias towards the coin landing on the same side as it started.”

The Moneyin2 Guide to Wealth

The Moneyin2 Guide to Wealth will get you the biggest return on your savings by maximising cash matches from your employer, free cash from the government, and shielding your investment gains from tax. It takes you step-by-step through the world of pensions, SIPPs, ISAs and ETFs — all in plain English.

More from Moneyin2:

Do you want Moneyin2 to recommend your Substack?

Get in touch at contact@moneyin2.com!

We want to hear from you!

What money issues do you want us to tackle in this newsletter? Let us know at contact@moneyin2.com.

Follow us on social media

Facebook, TikTok, Instagram, Twitter, and Threads.

Partner with us!

If you want to sponsor Moneyin2 get in contact here.