The ETF ‘bubble’

🔸 Plus: Art by KAWS goes up more than Banksy's 🔸 Billionaire Nick Candy pays a £161,000 service charge on his £175 million penthouse 🔸 What's the right amount of pocket money for kids?🔸

Your 2-minute guide to demystifying money and making you richer

The markets, year-to-date

S&P 500: 5,304.72 ⬆️ 11.85%

FTSE 100: 8,317.59 ⬆️ 7.57%

Bitcoin: $67,699.80 ⬆️ 53.15%

GBP to USD: $1.2773 ⬆️ 0.36%

GBP to EUR: €1.1742 ⬆️ 1.83%

Are passive investment ETFs causing a bubble in the stock market?

Harper’s Magazine has a long and interesting article about passive investing in exchange-traded funds, and whether it’s creating a dangerous bubble in the stock market.

(Harper’s is the American magazine favoured by liberal intellectuals, not to be confused with Harper’s Bazaar, the UK magazine read by fashion fans.)

The Harper’s theory is that so many people are now investing their retirement savings into funds that passively — and therefore mindlessly — track stock indexes that it is pumping up stocks in a way that is not rationally attached to their real value, and this is priming the market for a crash.

This issue is close to Moneyin2’s heart because, as regular readers know, we think that one of the smartest things you can do is invest in an S&P 500 ETF and passively let the market make you rich:

“Active” investors — professional money managers or people who buy and sell a lot — consistently fail to beat the market.

“Passive” investors — people who put their money into index-tracking funds that follow the broader market — tend to beat active investors in the long-run.

Trying to pick individual stocks — buying low and selling high, or jumping in and out of the market — is basically gambling and you should not do it.

In the long run, stocks go up. So you should invest in them if you’re serious about building wealth.

But as the Harper’s article says, passive investing via ETFs is massive enough to distort the market:

More than $15 trillion globally is now invested in ETFs.

Last year, the total size of US passive investments surpassed actively managed funds for the first time.

Passive’s share of the market is somewhere between 15% and 38% — which is a lot.

The article relies on a theory being pushed by Michael Green, the chief strategist at Simplify Asset Management, who has been banging this drum for a while.

If you’re a huge passive investing nerd — and guess what, that’s us at Mi2! —there’s a good episode of the Rational Reminder podcast here in which Green explains his theory at length, and with lots of detail about how the markets work. It’s well worth a listen.

This is Green’s theory:

Passive ETF investing has been successful, so lots of people do it.

So many people are doing it, largely via their pension plans (in the UK) and 401(k) plans (the US version of a private pension), that a significant chunk of the market now consists of asset management platforms that are always buying stocks come hell or high water.

Passive investors are “price insensitive”, he says. They don’t care if a company just disclosed bad news. They’re going to buy anyway, because they are investing for the long haul.

This is bad because investors should be sensitive to prices, Green says.

Large-scale price insensitivity is making the market “inelastic”, or unresponsive. The market no longer reacts in a sensible way to negative news because it’s just going up. It’s just going up because everyone is passively buying.

This makes the market “fragile”. If everyone wakes up one day and concludes that their savings are in stocks that are wildly overvalued, they’ll want to cash out quickly.

Imagine 100 million Americans all trying to sell at the same time.

It would be like a bank run — the market would not have enough liquidity to fill all the sell orders.

Green’s simulations think this could trigger an 85% crash in the market.

“The real risk is that you just end up shutting the markets. I realise that sounds insane but remember you have 100 million Americans and an untold number of people around the world who believe their deposits in the S&P 500 are safe. Take that away from them and they try to take that money out and suddenly the world changes in quite dramatic fashion.”

“A bank run can only be solved by shutting the bank.”

So far, so scary

There are good reasons to believe that Green is wrong.

The first is that ETFs have been popular for a couple of decades and they have been battle-tested.

From 2021 to 2022 the S&P 500 declined by about 24% — that’s a significant market correction and more than enough to shake out nervous investors.

There was a 32% decline in 2020 when the coronavirus pandemic shut down the world.

The 2008 financial crisis chopped about 50% off the market.

The dot-com crash of 2000-2002 was pretty nasty too.

After each event, the S&P dusted itself off, got back to its feet, and began climbing again. The declines, by definition, show that there are enough sellers capable of forcing a correction that revalues the entire market. And that will prevent bubbles.

Secondly, not everyone is invested in the same ETF. There are thousands of them. And not all these ETFs are plain-vanilla S&P 500 trackers. There are hundreds of ETFs that are “counter-programming” against the broader market, for people who think certain industrial or regional sectors will do better. Want an ETF for metals? There’s one for metals. Want an ETF for tech stocks? You got it. Want an ETF for Asian stocks? Knock yourself out. Green’s company offers a range of alternative ETFs if you want to bet on something that isn’t “the whole market”.

Lastly, there is a plausible scenario in which a lot of ETF holders may want to cash out. Baby boomers and Generation X-ers are in retirement or approaching retirement and they’ll want to finally spend all the money they’ve accumulated in their ETFs. So we may see a generational shift, with sizeable outflows from ETFs.

But they won’t all do it at the same time. That process will take decades to play out. And this demographic change is highly predictable — which means the active investors, probing for weaknesses, can price this into the market.

And Green admits that the bubble may be growing so slowly that he doesn’t know when it will burst. It may take so long that we’ll all be dead by the time it arrives, he says.

Our advice: It is difficult to imagine an event that would convince everyone they needed to get out of the entire market so suddenly that it would cause an 85% drawdown.

It would have to be an event more severe than the early days of the pandemic. Nuclear war? Nobody knows.

Just because you can’t imagine such an event doesn’t mean it won’t happen, of course. (No one thought that the mortgage market was in trouble in 2007. And yet the next year it derailed most of the planet’s banking system.)

But betting that an unimaginable event is more likely than a very plausible scenario (i.e. that the S&P will keep chugging along, as historic data suggests) is not a good thing to do with your personal wealth.

And for dessert …

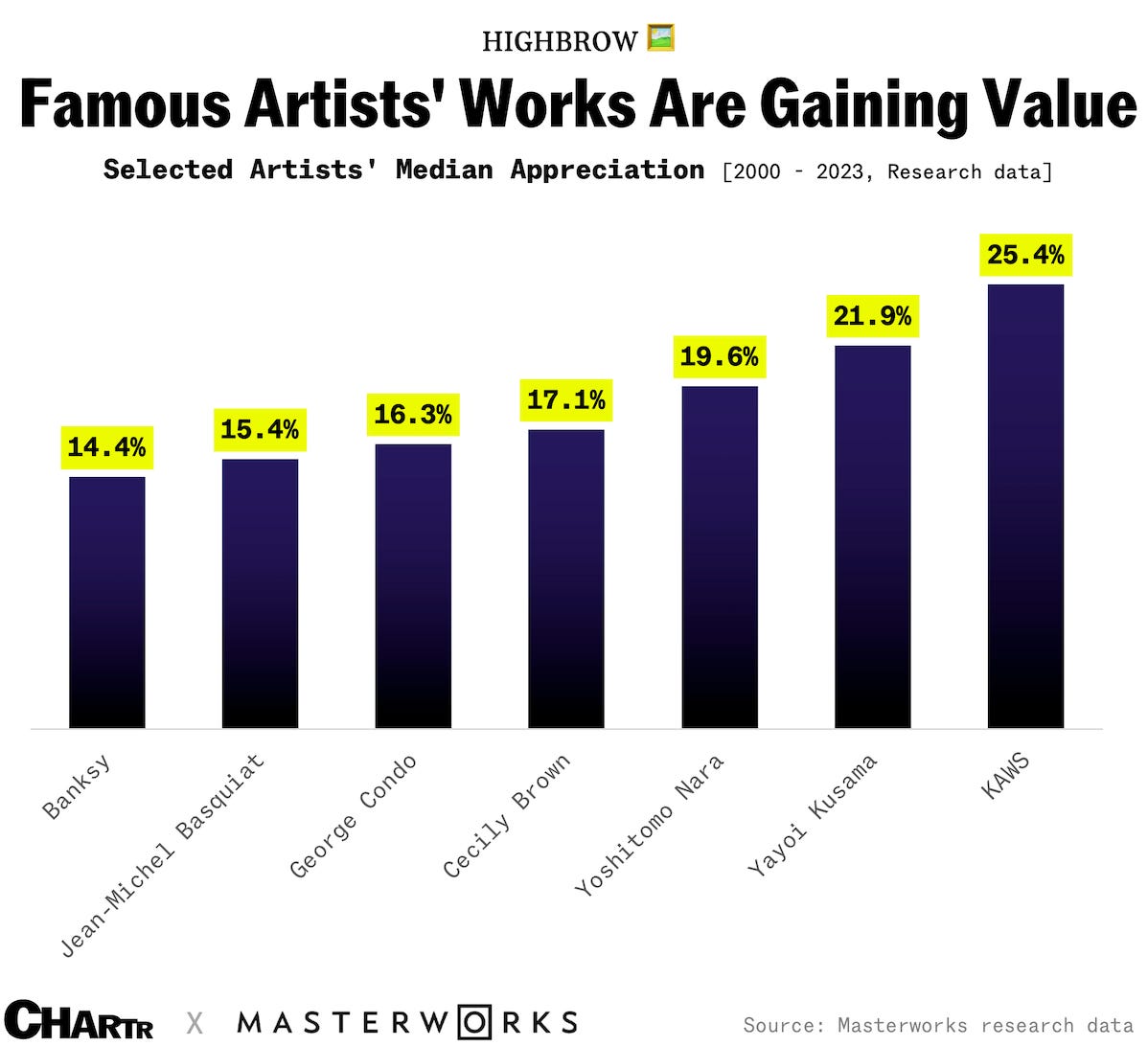

The value of art by KAWS has appreciated more than Banksy’s. The chart above comes from Masterworks, an art investment platform.

Why did Nvidia do a 10-1 stock split? Because with each share of the AI chip-maker now worth more than $1,000, they’re too expensive for many retail investors to buy.

Billionaire property developer Nick Candy spends only 20 days a year at his £175 million penthouse at One Hyde Park but nonetheless has to pay the £161,000 service charge. “The development has a private cinema, 21-metre lap pool, as well as sauna, gym, golf simulator, wine cellar, valet service and room service from the five-star Mandarin Oriental hotel next door,” The Guardian reports.

What’s the correct amount of pocket money to give your kids? Redditors are debating this issue here and discovering that a lot of people give their kids fixed budget debit cards.

41% of the S&P 500’s revenues come from outside the US. This is one reason Moneyin2 recommends investing in an S&P 500 ETF — you’re basically getting a little bit of everything, everywhere (and yes we know the S&P is dominated by tech giants).

“The markets just want to go up”. Some money managers are arguing that this year’s excellent stock market performance is based on mere momentum, not fundamentals.

More from Moneyin2:

We want to hear from you!

What money issues do you want us to tackle in this newsletter? Let us know at jim@moneyin2.com.

Follow us on social media

Facebook, TikTok, Instagram, Twitter, and Threads.

Partner with us!

If you want to sponsor Moneyin2 get in contact here.

Photo: Jim McCluskey.