The worst-case scenario for over-40s

🔸 Plus: Bands are boycotting festivals if they’re sponsored by Barclays 🔸 There’s a restaurant that banned men under 35 and women under 30 🔸 Inside "Big Chess" 🔸

Your 2-minute guide to demystifying money and making you richer

The markets, year-to-date

S&P 500: 5,433.74 ⬆️ 14.57%

FTSE 100: 8,163.67 ⬆️ 5.73%

Bitcoin: $67,109.70 ⬆️ 51.82%

GBP to USD: $1.2729 ⬆️ 0.019%

GBP to EUR: €1.1892 ⬆️ 3.13%

Is it too late to start investing in your 40s?

A reader sent Moneyin2 this message recently:

“Could you please consider a piece for those who have started investing late? 40s/50s?”

(First of all — we love your questions at Moneyin2! Keep them coming!)

This is a really great question because it’s a common issue: People don’t make much money in their 20s so they don’t save. Then maybe you have kids, which are expensive. Or you went back to university or retrained to switch careers.

Before you know it you’re in middle age and you have nothing saved.

And yet, retirement is looming — it’s “only” 20 years away!

The worst-case scenario

To think about this question, I decided to look at a worst-case scenario: What would happen if you started your saving and investing in your 40s at the worst possible time, when the stock market is at an all-time high, and cashed out to retire 20 years later into a market collapse, with stocks dipping 20% or more?

Turns out you’d do pretty well!

We know this because … this literally just happened.

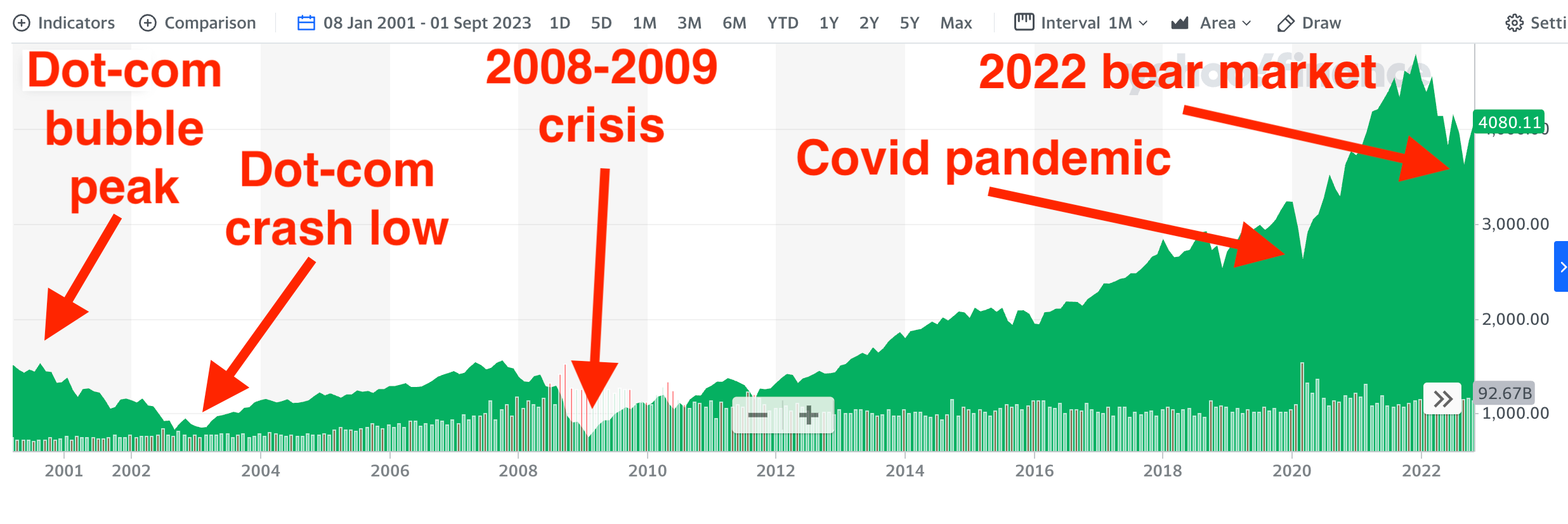

Here’s a chart showing the S&P 500 index of major stocks from the peak of the dot-com bubble in late 2000 to the bear market caused by Russia’s invasion of Ukraine in 2022:

Had you invested your life savings in 2000, you would have taken a hit in the dot-com crash, another hit in the 2008 financial crisis, a third hit in the pandemic and a fourth, humbling gut punch in 2022.

And you’d still have gains of 150%

You’d have more than that if you saved into your investments automatically, month after month, because your money would have bought more stocks than average as their value declined, giving you a magnified bounce upward when stocks went up.

This is called “pound-cost averaging” and it’s how you beat the market simply by being in it.

The government’s death calculator

The assumption I have made is that you’re in your 40s and you’re trying to retire 20 years later. In the old days that meant leaving work in your mid-60s, cashing out your savings and investments, and handing them to an annuity company in exchange for a guaranteed regular income for life. No more saving and investing for you! Just spend, spend, spend!

You can still do that. But life expectancy has changed, too. Sixty-six, the official UK retirement age, is no longer that “old”. In fact anyone who reaches 66 can expect to live 20 or 30 more years.

We know this because the government maintains a life expectancy calculator here. If you tell it your age it will give you an official estimate of when then government thinks you’ll die. Cheerful!

So you might want to stay invested, and let your savings continue to grow, well after you start using some of them as your retirement money. In other words, if you’re in your 40s you may still have an investment time horizon of 30 years or more.

How much will you need to retire?

There is no good answer to this question because it depends so heavily on your personal circumstances.

But there’s a great web site called Guiide that asks you seven basic questions about your personal financial circumstances and what you want to achieve. It takes about 10 minutes to complete and it will give you a very good estimate of how much you’ll need and when you’ll need it.

And, crucially, you can play around with the numbers.

🚀 Start now

When it comes to saving and investing, the most important asset you have is time. The longer your money works for you, the more it will make.

That’s because of a miraculous process called “compounding”, where your gains are added to your gains and those gains start making gains of their own, and so on, ad infinitum. Anyone who leaves their money in an investment that pays any kind of return, for a long time, will end up rich.

So, although you should not be discouraged about starting to invest in middle age, the very best course of action is to start in your 20s.

Compounding is one of the most important concepts in finance. And Moneyin2 has a whole post on it here.

Important practical stuff

In practical terms, you should follow the steps in the Moneyin2 Guide to Wealth. This will get you the biggest return on your savings by maximising cash matches from your employer, free cash from the government, and shielding your investment gains from tax. It takes you step-by-step through the world of pensions, SIPPs, ISAs and ETFs — all in plain English.

And for dessert …

Bands are boycotting festivals if they’re sponsored by Barclays. Latitude, Download, Great Escape, the Isle of Wight Festival, and Camp Bestival have all had bands pull out in protest at the bank’s alleged links to Israel. Barclays spends £112 million a year sponsoring music and denies that it invests in companies that make military products.

There’s a restaurant in St. Louis that has banned all men under 35 and all women under 30. The people who can get in think it’s awesome. Everyone else thinks it’s illegal.

Don’t hold your breath waiting for productivity improvements from AI. One economist estimates that AI will add only 0.66% in productivity growth over the next ten years — in total.

The S&P 500 index got reshuffled. Three new companies were added (private equity firm KKR, cybersecurity company CrowdStrike, and web site provider GoDaddy). They replaced recruitment firm Robert Half, US bank Comerica, and gene tech maker Illumina. Why is this interesting? Because if you’re invested in an S&P 500 ETF the index is sorting the best companies for you — no effort required.

The big money behind online chess. A fascinating longread about what happened to the game after computers learned to beat humans and humans learned to cheat.

Tesla shareholders voted “yes” to Elon Musk’s $55 billion payday, “the largest in human history”, according to Fortune.

Goldman Sachs owns a hotel. The Conrad in new York “has 463 rooms, all of which are suites. It also has something called the ‘Loopy Doopy Rooftop Bar,’ which serves the ‘Poptail cocktail.’ Suites usually cost from $665 to $3,027 a night,” according to Sarah Butcher.

More from Moneyin2:

Do you want Moneyin2 to recommend your Substack?

Get in touch at jim@moneyin2.com!

We want to hear from you!

What money issues do you want us to tackle in this newsletter? Let us know at jim@moneyin2.com.

Follow us on social media

Facebook, TikTok, Instagram, Twitter, and Threads.

Partner with us!

If you want to sponsor Moneyin2 get in contact here.

| A guest post by

|