“r > g”: What separates the rich from the rest of us

🔸 Plus: Accent bias is a real thing 🔸 Barclays stops sponsoring festivals 🔸 A bank fired some employees who pretended to work from home 🔸

Your 2-minute guide to demystifying money and making you richer

The markets, year-to-date

S&P 500: 5,431.60 ⬆️ 14.52%

FTSE 100: 8,146.86 ⬆️ 5.51%

Bitcoin: $67,109.70 ⬆️ 51.82%

GBP to USD: $1.2674 ⬇️ 0.44%

GBP to EUR: €1.1836 ⬆️ 2.64%

“r > g”: Where wealth and inequality come from

One of the most-read posts on Moneyin2 was published a couple of weeks ago, titled “The difference between rich and poor”. It explains a widely misunderstood fact of life: that wealth comes from owning assets, not receiving wages.

(At least I hope it was popular for that reason and not because it contained an anecdote about me trying to save money on food by sitting in a bathtub.)

Anyway! Simply stating that wealth comes from assets not wages doesn’t really prove it. So in this edition of Moneyin2 I’m going to explain why, statistically, owning assets makes you rich but earning wages does not.

The whole thing can be boiled down to an alarmingly simple mathematical expression:

r > g

Once you understand r > g, and how it affects your money, it can be life-changing.

But first, let’s recap the previous post on this topic:

The rich get their wealth from assets — stocks, bonds and property — whereas the rest of us get our wealth from wages.

The split between the people who have assets and the people who depend on wages is the driving force of inequality.

Thus waiting for your boss to pay you enough money to become rich isn’t a very good way to become rich.

Once you take this to heart you can begin to change your financial behaviour, by saving and investing for your future. Whether it’s stocks, bonds, mutual funds or property — having assets work for you rather than the other way around is the way to financial security and independence.

This all begs the question:

Why does this assets/wages divide make some people wealthy while others get left behind?

This is where r > g comes in. In this equation:

r = the rate of return on capital (i.e. assets like stocks, bonds and property).

g = the growth rate of the economy as a whole.

Thus r > g suggests that the rate of return (or growth) on capital is always greater than the growth rate of the economy.

The equation (and yes I know it’s technically an inequality not an equation but I am trying to keep it simple!) was developed by the French economist Thomas Piketty, who works at the London School of Economics. It is based on centuries of income tax data from the UK, US, France, Germany, Japan, and others.

OK, so how does this affect me, you ask?

It affects everyone who works for a living

Roughly 50% of all economic activity involves wages. The economy is a proxy for wages. If the economy is growing, wages are growing. If the economy shrinks, average wages are declining or wages are being paid to fewer people (i.e. unemployment is rising).

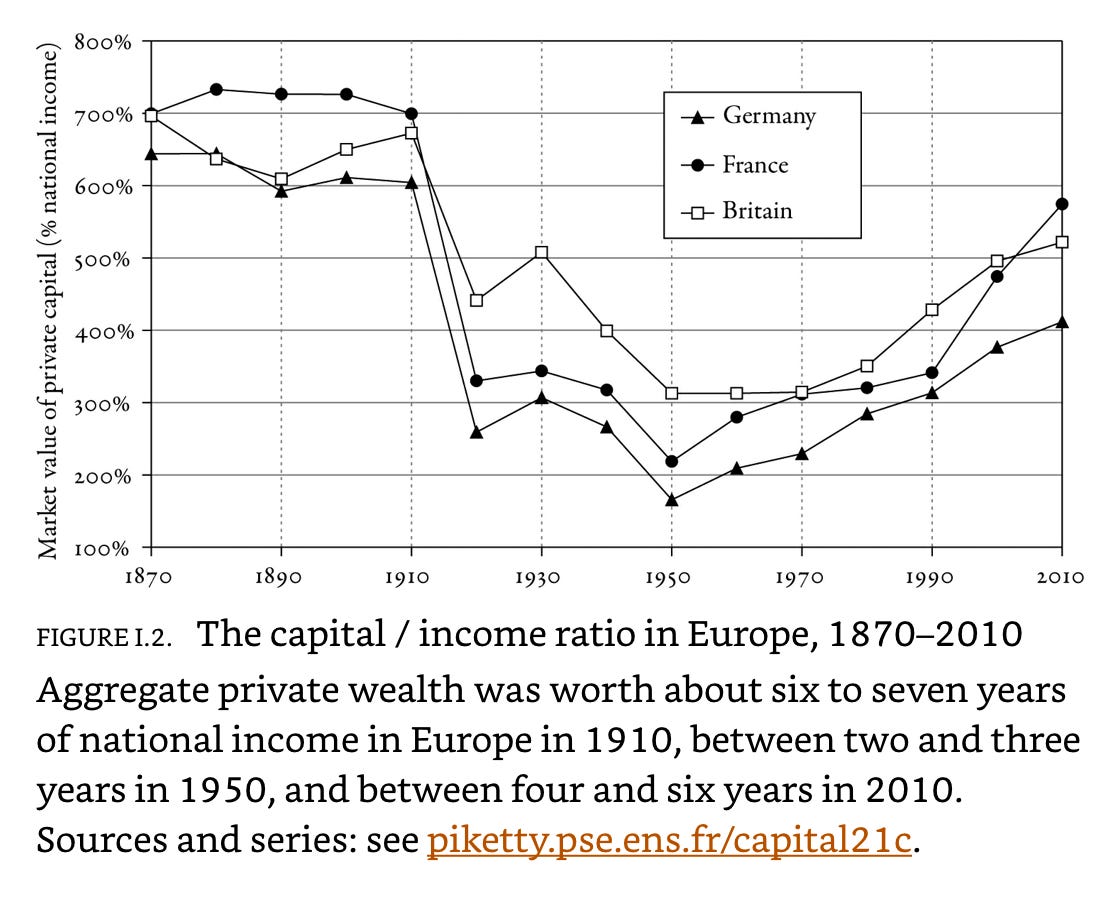

When Piketty looked at his tax data, he found that assets were always worth more than incomes. Here’s a typical chart:

And the rate of growth of capital (assets) was always higher than the rate of growth of the economy as a whole, he found.

In Q1 2024, for instance, GDP growth for the UK was 0.6% more than the previous quarter. By contrast, growth for the stocks in the FTSE 100 index was 3% — five times as much. This statistical relationship, that r is greater than g, has stayed true since modern income tax records began in the 1800s.

Now obviously you can get a pay rise. You can get a promotion. You can get a new job — and earn more money. A lot more money, if your career goes well.

But your cash comes to an end as soon as you lose your job. You take a break to raise kids. You’re sidelined by poor health. You followed your partner to a city where you have few connections and struggle to find work. Maybe you have to look after an elderly parent.

And, of course, there’s retirement.

Wages — always, always, always — come to an end

But assets don’t. They keep on working for you even when you’re asleep.

As we said last time, if you own assets:

When stocks go up, you get richer. When bonds make interest payments, you get richer. When you own a house, you get richer by living in it and letting its value rise on the market or renting it to someone else.

Yes, we know you can’t just snap your fingers and jump from the “wages” category to the “assets” category. But you can do it incrementally, month by month, by automating your saving, and investing those savings in a pension, ISA or SIPP.

Do you want to be a “g person” or an “r person”?

The decision is up to you, and Moneyin2 is happy to encourage and help you along the way.

Important practical stuff

The Moneyin2 Guide to Wealth will get you the biggest return on your savings by maximising cash matches from your employer, free cash from the government, and shielding your investment gains from tax. It takes you step-by-step through the world of pensions, SIPPs, ISAs and ETFs — all in plain English.

And for dessert …

Accent bias is a real thing. Some companies are encouraging recruiters to avoid discriminating against people who don’t speak RP English. Fascinating fact: In the last parliament 69% of Conservative MPs spoke in RP but only 37% of Labour MPs did.

Barclays has stopped its sponsorship of all UK music festivals following protests. Critics didn’t like that the bank provides financial services for defence contractors linked to Israel. The move ends £112 million a year in funding for live music events.

Wells Fargo fired a bunch of employees who pretended to work from home by faking keyboard activity on their computers. You can buy a “mouse jiggler” on Amazon for $10.

HMRC hasn’t fined a single person for enabling tax evasion in the last five years, despite a change in the law allowing it to do so.

The Euros have started and one financial analyst has dared to ask the crucial question: Does having sex before the game reduce an athlete’s performance? Yes, there is data on this, according to Joachim Klement.

More from Moneyin2:

Do you want Moneyin2 to recommend your Substack?

Get in touch at jim@moneyin2.com!

We want to hear from you!

What money issues do you want us to tackle in this newsletter? Let us know at jim@moneyin2.com.

Follow us on social media

Facebook, TikTok, Instagram, Twitter, and Threads.

Partner with us!

If you want to sponsor Moneyin2 get in contact here.

| A guest post by

|