Stay the hell away from 'AIM ISAs'

🔸 Plus: 500,000 millionaires will leave the UK by 2028, allegedly 🔸 Inflation is more expensive for the poor than the rich 🔸 A London-based AI trading firm is paying staff £3.6 million per head 🔸

Your 2-minute guide to demystifying money and making you richer

The markets, year-to-date

S&P 500: 5,408.42 ⬆️ 14.03%

FTSE 100: 8,181.47 ⬆️ 5.96%

Bitcoin: $53,429.15 ⬆️ 20.87%

GBP to USD: $1.3132 ⬆️ 3.18%

GBP to EUR: €1.1839 ⬆️ 2.67%

(as of market close on Friday)

Be very, very cautious about investing in AIM ISAs

A Moneyin2 reader recently asked:

“Should I invest in an ‘AIM ISA’ in order to help my kids avoid paying inheritance tax when I die?”

Spoiler alert: No!

We found this question fascinating because, frankly, we’d never heard of an “AIM ISA” before. After doing some research we now know why:

These tax-dodging vehicles are extremely risky and should be approached with caution at best and probably avoided altogether.

Put simply, an AIM ISA is a type of Stocks & Shares ISA which allows you to invest only in stocks traded on the UK’s AIM index, primarily for the purpose of taking advantage of a law that shields money invested in small UK companies from inheritance tax.

Yes, it’s complicated and slightly crazy

Let’s break it down.

What the hell is AIM?

AIM stands for “Alternative Investment Market” which is an index of publicly traded UK stocks for smaller companies on a sub-market of the London Stock Exchange.

There are some famous companies listed on AIM, such as Jet2, Asos, Boohoo, and YouGov. But there are also hundreds of crazy-sounding companies that no one has ever heard of. For example, Botswana Diamonds, which trades for 0.4p (literally a fraction of a penny) per share. The company searches for diamonds in — you guessed it — Botswana. It had revenue of only £15,000 last year.

Who knows? Maybe they will get lucky!

Companies whose shares are on AIM typically do not qualify to be on the main London Stock Exchange because:

They are too small.

Their shares are often priced in pennies.

They haven’t existed for a minimum of three years.

They don’t yet have a market value of £700,000 or more.

They may not have enough money to continue trading for more than a year.

So immediately you can see that AIM companies are smaller and therefore riskier than other types of shares. In the US these companies would be “penny stocks” that trade on the “pink sheets”.

The red flags are flying high, in other words.

What is an ‘AIM ISA’?

An AIM ISA operates in basically the same way as a regular Stocks & Shares ISA. (ISA stands for “individual savings account” but for some reason investment companies like to make everything sound as arcane as possible.)

An ISA allows you to save and invest money and keep all the gains tax-free, up to a yearly deposit limit of £20,000.

You can put your money into an ISA on any reputable investment platform and choose whatever funds or stocks you want. (Which? magazine has a ranking of the best ones here.)

An AIM ISA works the same way except that you’re restricted to only investing in companies on the AIM index and, when you die, your investments are not subject to inheritance tax.

So, obviously, if you have a bunch of money, and think you might die, and want to avoid having your kids pay inheritance tax, then an AIM ISA might start to sound tempting ...

Hold that thought.

Why does this weird loophole exist?

In 1976 the government noticed that many small family businesses collapsed or were broken up when the owner died because the children inheriting the business were forced to sell it to pay the inheritance tax. So the government changed the law so that small companies are shielded from inheritance tax, making it more likely that they can continue trading after the death of an owner.

Over time, this tax benefit — officially called “business relief” because everyone in finance hates normal words! — was extended to anyone who owned shares in smaller, qualifying companies.

Then in 2013 the law was changed again, to allow people to invest in AIM shares via an ISA. The result was a tax incentive that gooses demand for shares in small UK companies.

And now a small number of investment firms have taken advantage of all the above to create “AIM IHT ISAs”, which, as the name suggests, are ISAs that are specially crafted so they only invest in AIM shares that shield you from inheritance tax (IHT).

Unsurprisingly, AIM ISAs come with drawbacks:

AIM stocks are volatile. AIM companies frequently go bankrupt very suddenly. You can lose a lot of money betting on AIM.

Not every company on AIM qualifies for business relief, so you can’t just buy the whole AIM index through some kind of exchange-traded fund — which would be the easiest and safest way of investing in AIM companies. You have to figure out which companies qualify and then invest. Good luck with that!

Alternatively, you’ll need to open your AIM ISA with a professional money manager who can pick the stocks for you — and that will come with fees that eat into your gains.

You have to stay invested for two years before the inheritance tax shield kicks in.

Even if you or your money manager picks companies that qualify for business relief, the HMRC will still review your picks when your estate is wound up. And most investment managers say they can’t guarantee that all their picks will still be qualified come the fateful day.

AIM stocks can sometimes be difficult to sell because the market is so thinly traded.

You are restricted to small UK companies so you’re not getting the level of portfolio diversity that is healthy for someone trying to build wealth.

The government may change the tax law at any time. That is especially true now that we’ve got a new Labour government.

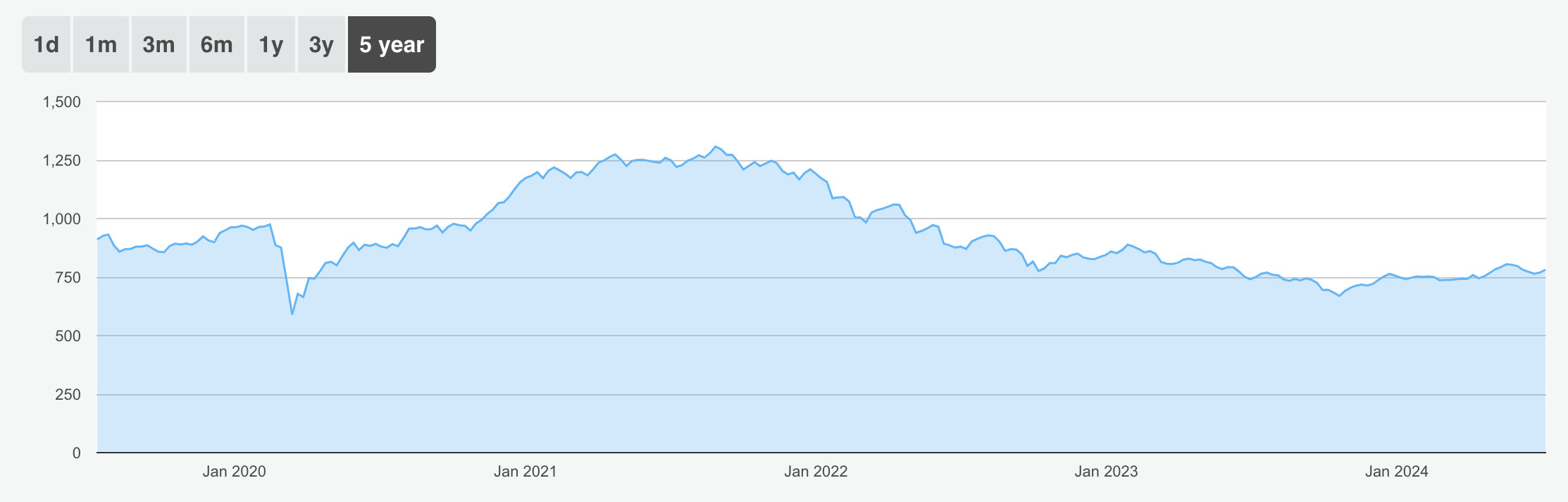

AIM is going nowhere

Lastly, there’s this: The historic performance of the AIM is dreadful. In the last 5 years it has gone nowhere:

That’s the whole index. Maybe the biggest AIM companies did better than the market as a whole?

Nope! The FTSE AIM UK 50 was also a disaster area over the last 5 years:

So… unless you have some very unique circumstances, don’t bother with an AIM ISA. They’re certainly nowhere near as good for building wealth and financial security as a Stocks & Shares ISA invested in a vanilla S&P 500 ETF. Sometimes boring is better.

Moneyin2 has a guide translating financial jargon here.

Moneyin2 has a post explaining the benefits of S&S ISAs here.

And for dessert …

500,000 millionaires will leave the UK by 2028, according to UBS. That’s a decline of 17%. The “non-doms” are looking for new places to not pay tax.

Inflation is more expensive for the poor than the rich. According to a new study of grocery prices, “prices of cheap goods grew between 1.3 to 1.9 times faster than the prices of more expensive brands”, the FT says. And even though it is possible to reduce your costs by switching brands or taking advantage of discounts, the cheap brands ultimately rose higher in price percentage-wise than the expensive ones.

A London-based automated trading firm (aka they use AI to make trades) is paying staff £3.6 million per head in annual compensation. That’s more than Jane Street, the secretive investment firm that pays notoriously well.

Substack writer Darnell Mayberry collects his first $1,000 in dividends. Here is how he did it.

US tax authorities went after 1,600 millionaires whom they believed were dodging their taxes. They recovered $1 billion.

The Moneyin2 Guide to Wealth

The Moneyin2 Guide to Wealth will get you the biggest return on your savings by maximising cash matches from your employer, free cash from the government, and shielding your investment gains from tax. It takes you step-by-step through the world of pensions, SIPPs, ISAs and ETFs — all in plain English.

More from Moneyin2:

Do you want Moneyin2 to recommend your Substack?

Get in touch at contact@moneyin2.com!

We want to hear from you!

What money issues do you want us to tackle in this newsletter? Let us know at contact@moneyin2.com.

Follow us on social media

Facebook, TikTok, Instagram, Twitter, and Threads.

Partner with us!

If you want to sponsor Moneyin2 get in contact here.