Premium bonds are terrible

Premium bonds are terrible

🔸 Plus: A TikTok influencer is telling people to trade stocks based on tarot cards 🔸 Gen-Z thinks being 10 minutes late is the same as being on time 🔸 Citi staff are gossiping about their CEO 🔸

Your 2-minute guide to demystifying money and making you richer

The markets, year-to-date

S&P 500: 5,477.90 ⬆️ 15.50%

FTSE 100: 15.50 ⬆️ 6.47%

Bitcoin: $60,725.50 ⬆️ 37.37%

GBP to USD: $1.2634 ⬇️ 0.73%

GBP to EUR: €1.1818 ⬆️ 2.49%

Premium bonds, and why they are bad

Whenever someone starts talking about premium bonds my blood pressure goes up. It’s always the same: “My friend won £10,000 on the premium bonds!”

So, are premium bonds a good investment?

No.

No, they are not.

Premium bonds are neither “premium” nor “bonds” and smart investors stay the hell away from them.

Premium bonds are based on false advertising

Premium bonds are actually a monthly lottery run by the National Savings & Investment bank. You buy a “bond” from NS&I for a minimum of £25 and the government pays interest to NS&I — not to you — on the money collectively “invested” in premium bonds.

Currently, that interest rate is 4.4%. Which doesn’t sound too bad. But that interest isn’t going to you, the person who bought the premium bond. It’s going to NS&I. That organisation then takes the interest and uses it for cash prizes in a series of draws, exactly like a lottery, every month, to random bond holders.

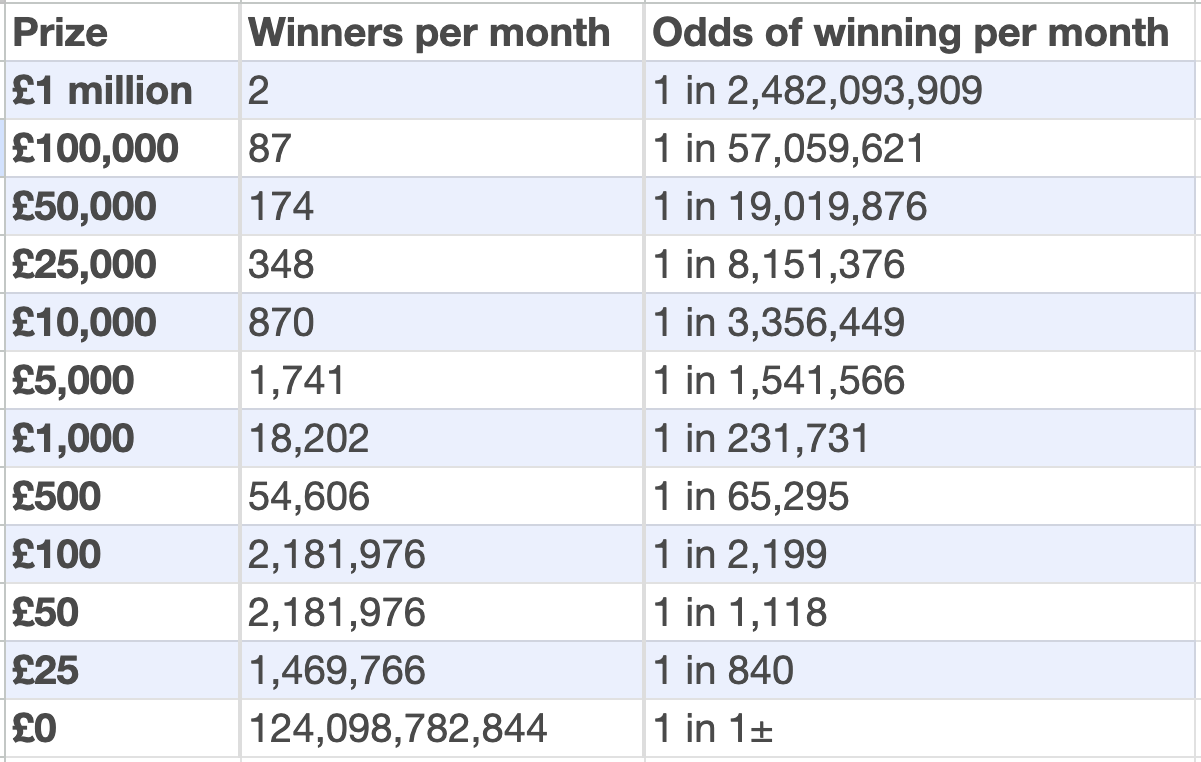

Your chances of winning any money in this lottery are 21,000 to 1. It says so on the NS&I web site. (At least they are honest about it.)

But those are the average odds. There’s a helpful table here of the odds for winning each type of prize. Crucially, the best odds, for winning the smallest prize (£25), are 840 to 1. For a lottery that’s not bad. But for a return on your savings it’s absolutely terrible.

Your chances of winning the £1 million jackpot are 2.5 million to 1.

Premium bonds are only “bonds” in a technical sense. It is true that you have paid money to a bank, and the bank is offering you a return on that money. But the return is in the format of a ticket to a lottery that you are unlikely to win.

It’s a rip-off, in other words

In the grown-up world, bonds do not work like this. A bond usually looks like a loan: You pay (lend) some money to a bank and in return the bank promises to give you a stream of interest payments. The bank gets money to invest in the short-term and you get even more money in the long-term.

That is not what is happening with premium bonds, because NS&I is not giving you any interest at all. Money held in premium bonds might as well be stashed under your mattress. There is nothing “premium” about them because the return on premium bonds is usually less than the return on actual bonds.

So why do people ‘invest’ in premium bonds?

NS&I has done something very clever and very misleading: Every month, about 5.8 million premium bonds do receive a prize payout. The vast majority of those prizes are £100 or less. But about 20,000 bonds win £1,000 or more every month.

That generates a constant pool of people — thousands per month — who tell their friends and family about their amazing premium bond win.

That’s why you’re always hearing about “a friend of a friend” who won money on the premium bonds.

British people are gambling addicts, and this constant word-of-mouth chatter about premium bond wins is like crack to a cokehead.

The actual odds of you winning £1,000 or more are 232,000 to 1:

Again, terrible odds.

Premium bonds function like a tax on people who didn’t pay attention in maths class, basically.

Yes it is true that you don’t lose money in this lottery. Your premium bonds sit there like cash in an account paying 0% interest and you can get that money back anytime. That is the only good thing about premium bonds. But if you’re storing cash in a place that pays 0% interest you’re losing money every month as inflation eats away its value.

And for dessert …

TikTok influencer uses tarot cards to guide her day trading. Do not do this.

Scottish people believe they need a salary of more than £106,000 to feel rich but folks in Yorkshire need only £86,000, according to a survey by Indeed.

A group of London-based Citi employees are using the comments sections of Wall Street Journal articles to criticise the bank’s CEO, Jane Fraser.

Bulgaria and Romania failed tests to switch their currencies to the euro. Both countries had inflation that was too high.

Gen-Z employees think that being 10 minutes late is the same as being on time.

There’s a weird glitch in the schedule for when the UK minimum pension age changes. The age at which you can start tapping your work pension or SIPP will increase from 55 to 57 on 6 April 2028: But … “The legislation as written will allow some to access their pension at age 55, but then lock them out again because they won’t be 57 when the pension age rises!” according to The Monevator. One million people could be affected.

People are increasingly refusing to switch on their cameras or activate their microphones in virtual meetings, according to HBR.

More from Moneyin2:

Do you want Moneyin2 to recommend your Substack?

Get in touch at jim@moneyin2.com!

We want to hear from you!

What money issues do you want us to tackle in this newsletter? Let us know at jim@moneyin2.com.

Follow us on social media

Facebook, TikTok, Instagram, Twitter, and Threads.

Partner with us!

If you want to sponsor Moneyin2 get in contact here.