The 'Jaws' problem: You’re going to need a bigger boat

🔸 Plus: A list of “non-dom” millionaires who have fled the UK 🔸 Why bear markets are good for you (eventually) 🔸 What happens when you lend a friend money and they don't pay you back 🔸

Your 2-minute guide to demystifying money and making you richer

There’s a famous moment in Steven Spielberg’s “Jaws” where the main character, police chief Martin Brody, comes face-to-face with the shark for the first time. Terrified, he walks backwards into the cabin of Quint, the obsessive shark hunter who plans to reel in the monstrous fish, and says, “You’re going to need a bigger boat”.

The line was never in the original script — actor Roy Scheider ad-libbed it based on an in-joke among the film crew about how small Spielberg’s budget for the movie was.

On the topic of budgets being too small, you might have had a similar feeling if you saw the recent update from the Pensions and Lifetime Savings Association, which produced a set of updated numbers on how much money Brits will need annually to retire comfortably. A single person will need £43,900 a year; a couple will need £60,600, the PLSA says.

There’s only one problem, according to the wealth management firm Quilter. In order to fund guaranteed lifetime income at that level, a single person would need to buy an annuity costing about £805,000. A couple would need nearly £1 million between them. (An annuity is a type of insurance plan in which you give a company a lump sum and in return they guarantee you a stream of payments for as long as you live.)

£805,000 will require a bigger boat

Whether you need — or even want — to fund your entire retirement with an annuity is a separate issue, of course. But the question remains: What percentage of your salary do you need to save to get to that Jaws-esque number, ensuring you don't outlive your money? Advisor Perspectives recently published a study on that topic from academics William Bernstein and Edward McQuarrie. Their calculations show that the usual advice — save 15% of your income and invest in a mixture of stocks and bonds — will likely come nowhere near to producing enough money.

In reality, they argue, most people should be saving something like 25% or more of their income. They also argue that holding bonds — which are usually thrown into the mix to soften declines in the stock market — actually hurts your results. (Moneyin2 did a post on why this is so here.) You might be able to squeak over the line if you save 15% but are invested in 100% stocks, the authors say.

In Britain, your employer has a legal duty to offer you a workplace pension plan into which, at a minimum, your employer will contribute 3% of your salary and you must contribute 5%, giving you an 8% savings rate. (Workplace pensions are the single best way to save, invest and secure your financial future and Moneyin2 did a post detailing why that is here.)

But clearly, 8% is nowhere near enough for most people to get to £805,000. You’ll need to contribute much more than the minimum 5% if you want financial independence.

Enter the Australians

There’s one country that has gone a long way to fixing this: Australia. In the Australian “superannuation” system, which works in a similar way to the UK system, the required employer contribution is 11.5% and will rise to 12% soon. Like the UK, employees are able to contribute as much as they like up to certain limits. Notably, with a 12% employer contribution rate, an employee need contribute only 13% of their income to hit the 25% level they would need to reach that £805,000 goal.

It’s sobering, for sure. But ignorance is not bliss when it comes to personal finance. And that’s why the Moneyin2 Guide to Wealth exists: To walk you through it.

The Moneyin2 Guide to Wealth

The Moneyin2 Guide to Wealth will get you the biggest return on your savings by maximising cash matches from your employer, free cash from the government, and shielding your investment gains from tax. It takes you step-by-step through the world of pensions, SIPPs, ISAs and ETFs — all in plain English.

And for dessert …

Bear markets are your friend. An amazing set of charts from Ben Carlson that show, over the long run, that investors are near-guaranteed to take a hit in a bear market and also near-guaranteed to see gains on their investments anyway.

A partial list of “non-dom” millionaires who have fled the UK since the Labour government abolished their tax breaks, from City AM.

Most Brits probably don’t realise that their pensions are frozen if they move abroad.

What happens when you lend a friend money and he or she doesn’t pay you back. A Reddit thread on a remarkably common problem.

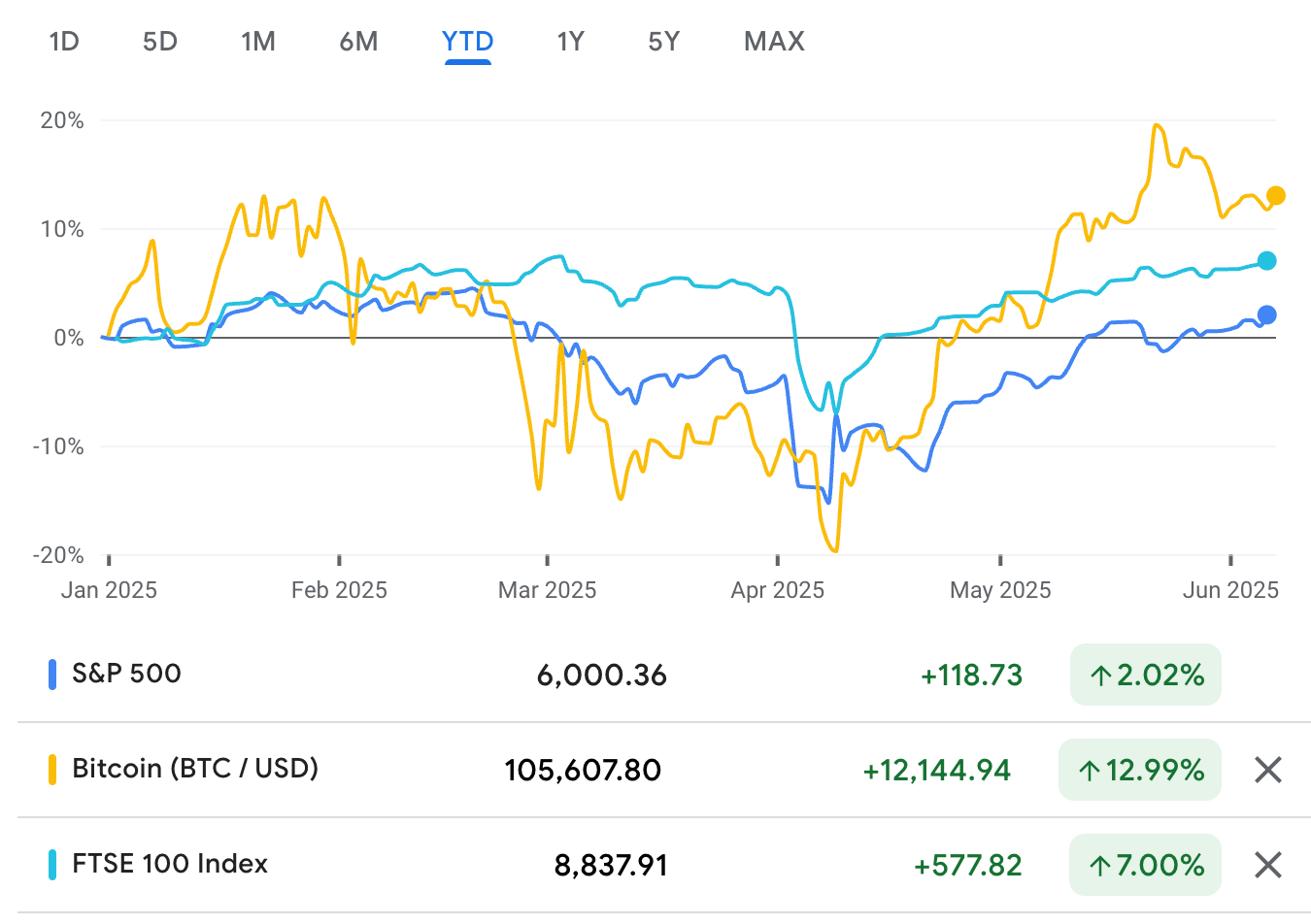

The markets, year-to-date

More from Moneyin2:

Do you want Moneyin2 to recommend your Substack?

Get in touch at contact@moneyin2.com!

We want to hear from you!

What money issues do you want us to tackle in this newsletter? Let us know at contact@moneyin2.com.

Follow us on social media

Facebook, TikTok, Instagram, Twitter, and Threads.

Partner with us!

If you want to sponsor Moneyin2 get in contact here.